It is not easy being a bank in Brazil. Itau Unibanco’s (NYSE:ITUB) latest income statements can be a testament to this with the financial services firm reeling from a pandemic induced cratering of the Brazilian economy.

With consumer credit a key driver of business growth for the $54B Sao Paulo based lender, it can be easy to see how depleted revenues are only now recently on the mend.

Brazil – the Latin American juggernaut – has been floored by the SARS-Cov2 pandemic. The colorful Lusophone nation of 210 million inhabitants persistently faces an array of political, economic and social hurdles. Political wrangling and growing discontent with the Bolsonaro regime, have been central to many of the country’s challenges.

Structural economic woes and inflationary pressures adversely impacting the Brazilian Real continue to hamper the country’s growth perspectives. A pervasive corruption scandal involving national energy darling Petrobras (PBR) matched with spiraling energy costs, and growing discontent among Trade Union groups all paint a rather grim picture.

25-year GDP annual growth rate Brazil

Source: Trading economics

Looking at 25 years of Brazilian growth rate data underscores the sizable impasses the country has traversed. The collapse of the global banking system did not leave the country unscathed. Nor did the jarring corruption scandal which unfolded around 2015. Lastly, the SARS-Cov2 pandemic pushed the country to the edge of the economic abyss, only for the country to bounce back subsequently. But is this bounce a stimulative fueled one which is transient?

Not all is bad for the Brazilian economy. The country remains a commodity powerhouse exporting everything from oil, iron ore, coffee, sugar cane, cattle, and oranges and is likely to benefit from any commodity super-cycle, should one eventuate.

Itau Unibanco presents its earnings on 2 August providing an interesting Segway into understanding how these different macro-economic challenges are impacting the country’s financial system.

Itau Unibanco is the result of a 2008 marriage between rival Brazilian banking enterprises Banco Itau and Unibanco. The Brazilian banking juggernaut provides a range of financial products and services in Brazil and abroad via 3 distinguishable segments – retail banking, wholesale banking and corporate/ institutional banking.

Like many banks, the venture provides deposit products, loans, credit cards, investment banking services, mortgage brokering, credit and investment services, and foreign exchange brokerage.

Beyond the routine banking products offered, the Brazilian financial services venture also markets property and casualty insurance, life insurance and reinsurance products. With traditional historical roots in Sao Paulo, arguably Brazil’s financial center, the company was founded in 1924.

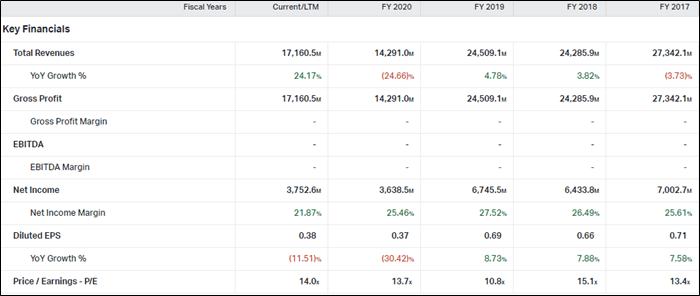

Key Financials – Itau Unibanco with all data converted to US $

Source: Koyfin

Key financial data for the Brazilian lender emphasizes the economic tumult faced over the past couple of years. With a Covid-induced decline in economic activity which translated to a $10B reduction in sales (-25%) from 2019 to 2020, only now is the company slowly recovering.

Current sales revenues are now off the pandemic-driven lows with the bank commendably managing to maintain profit margins despite noticeable stunted growth on a diluted earnings per share basis.

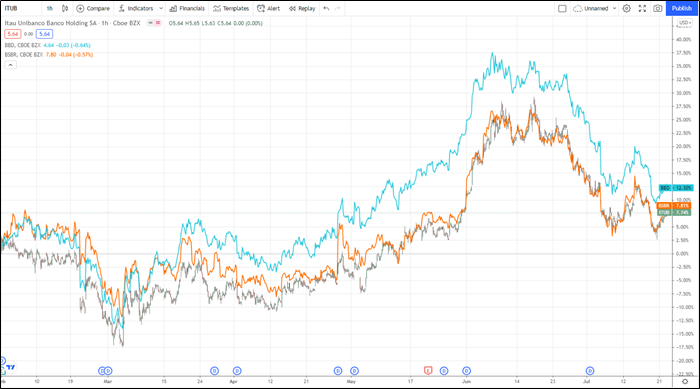

Year-to-date total return profile – ITUB v BBD v BSBR

Source: Tradingview

Year-to-date price action for the big Brazilian banks has been decidedly correlative, with Banco Bradesco SA (BBD) leading the peer group (+12.30%). Banco Santander Brasil SA (BSBR) and Itau Unibanco Holding SA have had rather indistinguishable total returns – with the former (+7.81%) outperforming by solely 7 basis points. Nothing to get too excited about.

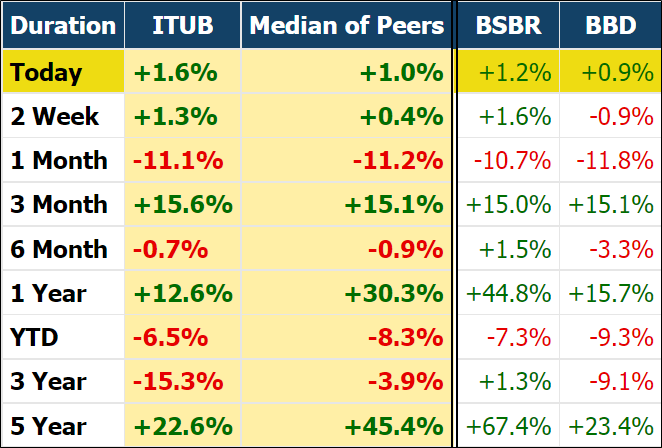

Price performance ITUB v BSBR v BBD

Source: Market Chameleon

If anything, the real standout in the basket of peers has been the long-term returns story of Banco Santander Brasil SA which has managed to post gains of ~45% over a one-year period and +67% over 5 years. Contrasted against the Brazilian banking peer group, Itau Unibanco Holding SA has given us little to write home about, with paltry returns of +12% over one year and only +23% over the longer 5-year holding period.

The investment community is anticipating the Brazilian banks earnings which are presently penned in for 2 August. On the same date, the corporation goes ex-dividend, with a distribution of $0.003 per common share – the equivalent of an annual dividend yield of 1.2%.

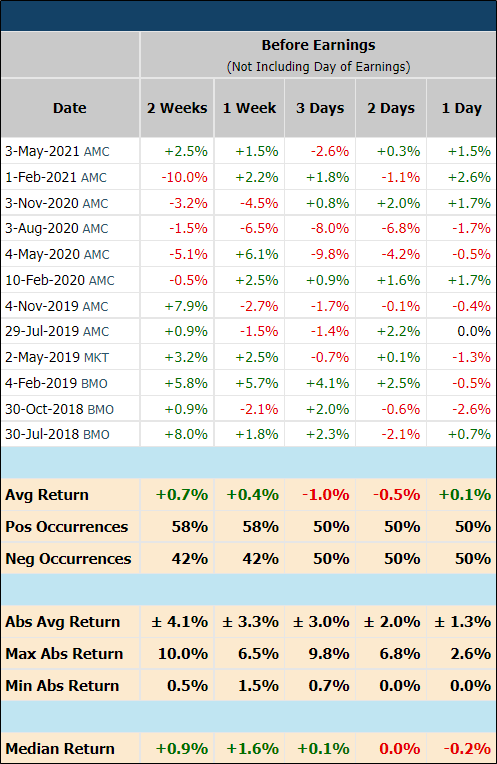

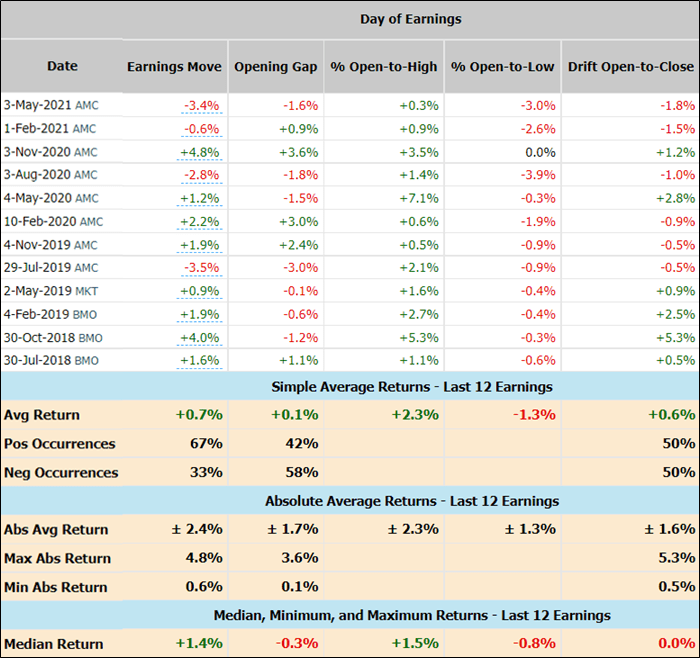

It remains challenging to draw any meaningful conclusions on future price action on the run-up to earning by scrutinizing historical data. If anything, negative observations have gradually crept into the data feed on the days just before earnings with negative median returns both 2 days and 1 day out from the announcement, respectively.

Another observation is that big positive gains appear to be a thing of the past for the Brazilian bank on the 2-week run-up to the event – Over the last 4 quarters, the biggest positive gain has been around +2.5% measurably outgunned by more meaningful negative returns (-10% – 2 weeks out from day of earnings earlier this year) More recently, the moves to the downside appear to be more accentuated, even if they only occur roughly as often as positive ones.

Historical price action on run into earnings – ITUB

Source: Market Chameleon

The price action on day of earnings distinguishes itself from the indifferent positive and negative observations on the run-up to the event – even if negative observations appear more pronounced.

Historical price action on day of earnings – ITUB

Source: Market Chameleon

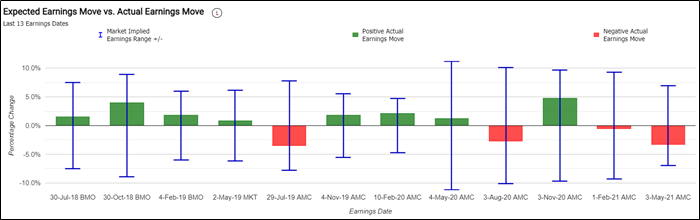

The biggest standout among all the data sets linked to earnings events for Itau Unibanco Holding SA has been the consistent overpricing of movement in the stock implied by the options market.

During the most recent earnings period on 3 May 2021, options prices anticipated a +/- 7.0% post earnings move, compared to an actual move of -3.4%. Over the past 13 quarters of data, options pricing has systematically overcooked the move in price action.

On average, the predicted move after earnings announcement was +/- 7.6% when, in fact, actual moves in absolute terms solely amounted to 2.6%. This is a sizable overestimation and, volatility willing, primes the stock as a candidate for either iron condors or iron butterflies going into the event.

Expected earnings move vs actual earnings move – ITUB

Source: Market Chameleon

The flip side of developing a direction-neutral options strategy to capitalize on the earnings event is that (unfortunately) the historical volatility crush observed has been extremely low. On average that volatility crush has only been 5% making it a somewhat inappropriate candidate for volatility traders.

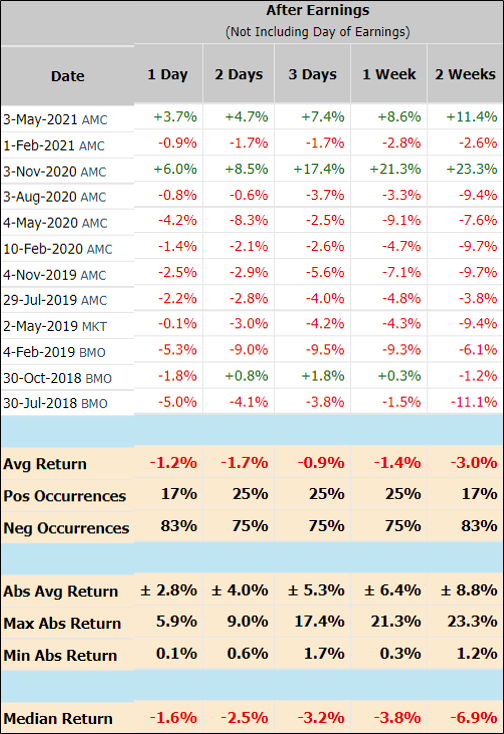

Data following the quarterly earnings report has been surprisingly consistent – in being negative.

Historical price action on day of earnings – ITUB

Source: Market Chameleon

As we have observed trawling through historical data, directional risk for the stock price during earnings navigates several stages – price action into the event has been relatively difficult to call with a skew possibly to the negative side, at least during most recent observations.

Big gains on the run-up to the event also appear to be a thing of the past. On the day of the earnings event, a more positive skew appears across the data sets. 67% of the time, the earnings move has been positive.

More remarkably, the moves post earnings seem to provide us the most consistency – save 2 big outliers, the data is almost wholly negative, with the stock languishing invariably following the earnings report.

Another consistency manifests itself in the extent to which options prices overcook anticipated moves. Over 13 quarters of data, we are yet to see the stock price directionally blow through anticipated price action brackets which can be calculated from options prices.

Seemingly, big moves in the underlying are persistently anticipated but rarely manifest themselves, making Itau Unibanco Holding SA (ITUB) a perfect iron condor/ iron butterfly candidate if only there were sufficient volatility to sell.

My long-term outlook on the stock remains bullish – with the bank a barometer of the economic wellbeing of the Brazilian economy, reality is the country (along with the rest of Latin America) is coming from a long way back.

While the country continues to wobble from the implications of an extensive health pandemic, enduring growth opportunities for a largely commodity focused economy persist.

On a more near-term basis, I remain directionally neutral – hard to say where the stock price will go during this next earnings report, save that consistently real moves have been significantly more muted than anticipated ones.

This article was written by

Disclosure: I/we have a beneficial long position in the shares of PBR either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.